Rose Lincoln/Harvard Staff Photographer

Work & Economy

New economic tracker finds flaws in U.S. recovery plan

Opportunity Insights report suggests targeted social insurance programs may be more effective

Results from a new economic tracker that looks at real-time statistics on consumer spending, jobs, and business revenue suggest that the government’s traditional recovery strategies to reverse the downturn triggered by the pandemic are not having a major impact, because they fail to address the root of the problem — consumer fear of the virus itself.

The findings, summarized in a report published Wednesday by Harvard’s Opportunity Insights group, suggest that the only way to fully revive the economy is to address the virus itself through therapy or a vaccine. And in the meantime, barring some other medical advance or shift in the economy, a more effective approach would be to focus on bolstering the businesses, individuals, and areas most affected, instead of broad-based solutions like direct stimulus payments to all Americans.

“The question is: Are you going to approach this as are we going to stimulate the economy and try to get it back on track with economic policy? Or are we going to look at this as what economists would call social insurance?” said Raj Chetty, William A. Ackman Professor of Public Economics and director of Opportunity Insights, an institute of social scientists and policy analysts who harness big data for policy solutions.

“Those are two fundamentally different views. One view is we’re going to restart the economy and get it back to where it was through economic policy. My instinct is: That’s just not possible, because you can’t make people go out and spend and go out and do what they were doing before if they’re fundamentally just worried about their health. … I think you can take the perspective of: We need to help people who need to feed their families, need to be able to pay rent, need to be able to pay their utility bills, and so forth. We do that through unemployment benefits, through the food stamp program, through things like Medicaid that provides health insurance coverage in these times.”

The Opportunity Insights Economic Tracker uses data from credit card processors, payroll firms, and financial services firms. It is an interactive tool launched in May to help policymakers assess the effects of the downturn in real time and evaluate policy impacts in different geographic regions of the U.S. at a granular level. The tool is open to and free for public use.

“The rich cut back; the poor end up bearing the consequences.”

Raj Chetty, director of Opportunity Insights

In the report, the Opportunity Insights team — which includes Co-Directors Nathaniel Hendren, a Harvard professor of economics, and John Friedman, a professor of economics and international and public affairs at Brown University, along with Michael Stepner, an economist who completed his Ph.D. at MIT last year — highlights the effects the novel coronavirus has had on consumer spending and employment rates, and evaluates the policies intended to stabilize them during the collapse.

U.S. government statistics show almost all of the reduction in the nation’s GDP came from a sharp drop in consumer spending, which accounts for more than two-thirds of the economy. So the group began by studying this drop and analyzing the impacts of those reductions on businesses and workers.

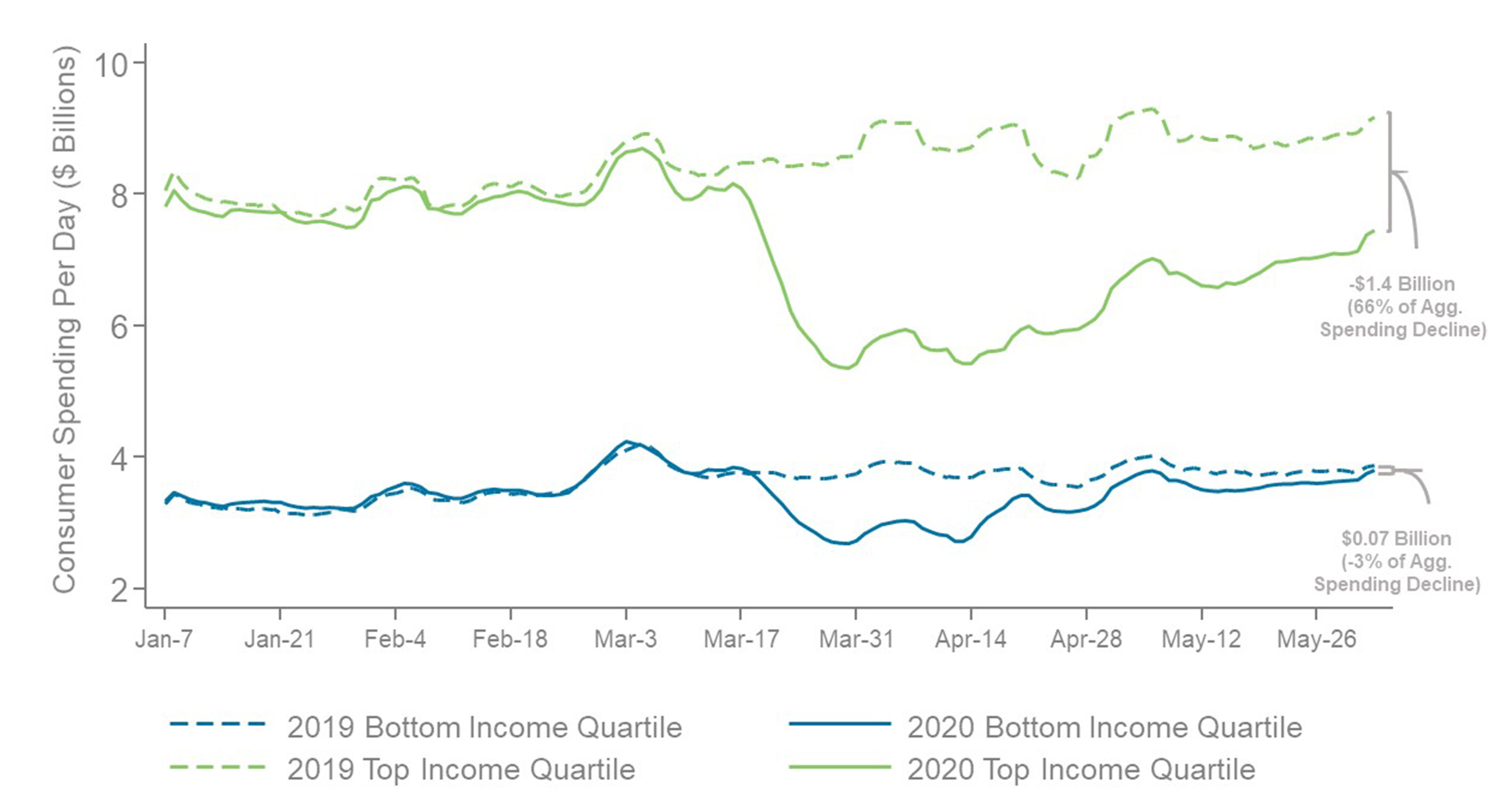

They discovered that high income households accounted for most of the drop in consumer spending and that small businesses in higher-income areas had suffered greater revenue declines and more losses of low-wage workers than their counterparts in less-affluent ZIP codes. In fact, two-thirds of the total drop in credit-card spending between January and the end of May came from households in the top 25 percent of the income distribution, while households in the bottom 25 percent spent at the same levels they had before the crisis.

Consumer spending during COVID-19 crisis, by income group.

Opportunity Insights

This decline in spending by the rich differs drastically from previous recessions, when there wasn’t a health risk like the coronavirus, suggesting the change was largely driven by health concerns rather than any financial reason. The tracker found that decreases in spending were most pronounced in businesses that require in-person interaction, such as restaurants, transportation, and salons. Many high-income households did not lower their spending on services that don’t require interaction, such as landscaping.

The fallout was apparent. Small businesses in the most-affluent ZIP codes lost more than 70 percent of their revenue, compared with 30 percent in lower-income areas from January to April. As those businesses lost revenue, they laid off workers at higher rates. According the tracker, in high–rent areas more than 70 percent of workers at small businesses were laid off in the two weeks after the pandemic began. In that same period, fewer than 30 percent of workers in the ZIP codes with the lowest rents lost jobs. In San Francisco, for example, job losses for low-income workers were higher in affluent neighborhoods such as Nob Hill than in lower-income places like Bayview.

Chetty stressed that it’s the low-income workers who are bearing the brunt of the current economic shock and that it illustrates the interconnected economy. “The rich cut back; the poor end up bearing the consequences,” he said.

The researchers then trained their eyes on the effects of state-mandated openings and the policies the federal government implemented to mitigate the economic fallout.

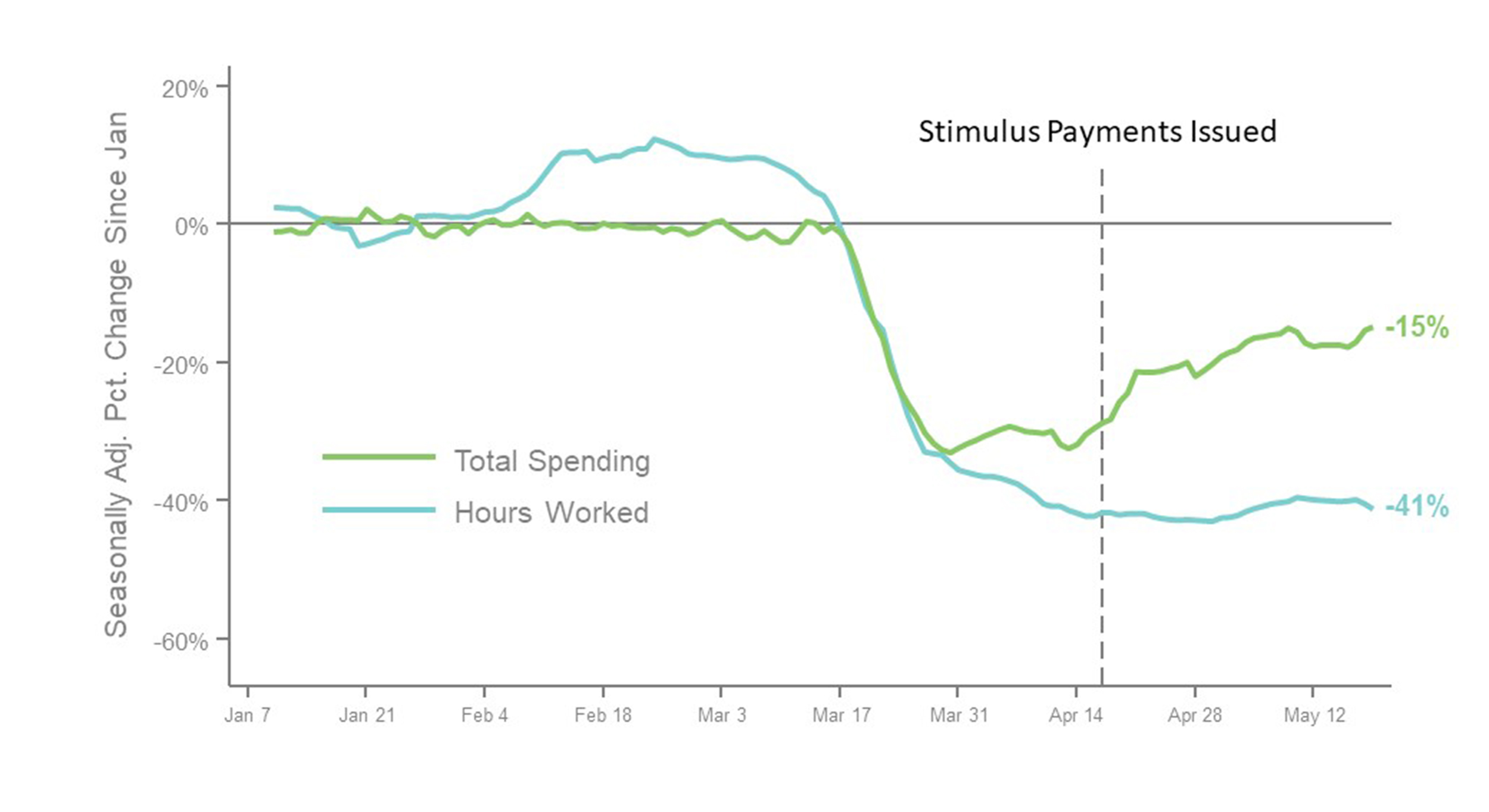

States that have begun reopening, even the earliest to do so, have seen only modest gains, and stimulus payments to individuals and loans to small businesses have not led to a surge in either revenue or employment rates for those firms most affected. Instead, most of the jump in consumer spending from stimulus payments went to goods from delivery services, like Amazon, that require no human contact.

Stimulus checks fail to buoy total spending or payrolls.

Opportunity Insights

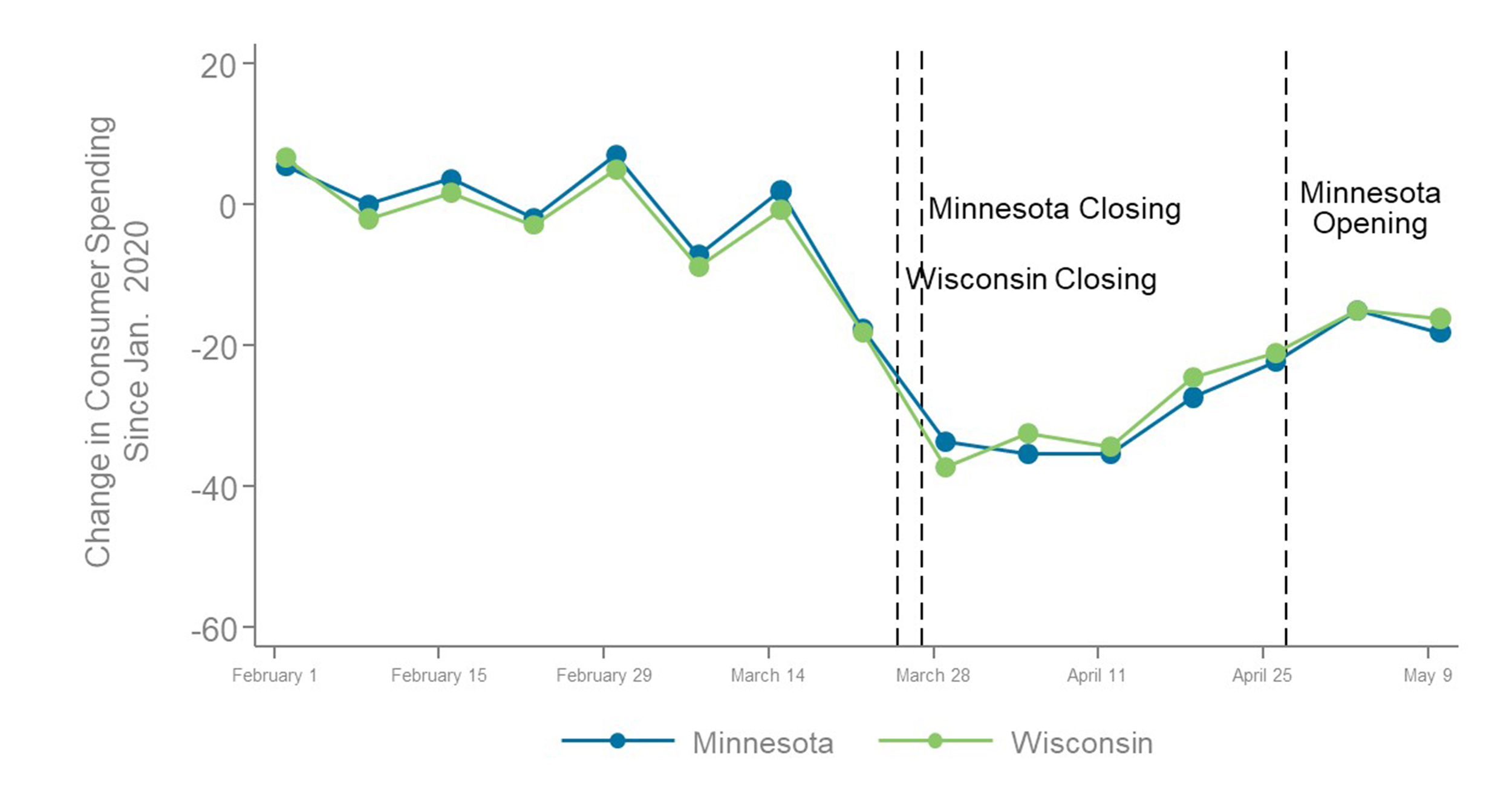

The group also found little difference in the economic improvement of states that opened as early as April 20 compared with peers that remained closed to the end of May. For example, spending in Minnesota and Wisconsin were about the same from February through May, even though Minnesota began opening nonessential business on April 27 and Wisconsin delayed until May 13. The same holds true for their employment rates.

Despite reopening sooner, Minnesota has seen similar spending levels as Wisconsin.

Opportunity Insights

Looking at the $300 billion CARES Act, the data show there was a spike in consumer spending after April 15 when deposits from the stimulus package first started hitting Americans’ bank accounts. The increase was greatest among low-income households overall, but the jump did not translate into a rise in employment in many areas because the additional spending went largely to national delivery services, not the beleaguered in-person businesses that needed it most. As a result, employment of low-income workers remained down 41.9 percent at the end of April despite total spending as of May 12 being down only 15 percent from pre-pandemic levels. Small-business revenue is down 18 percent, according to the tracker.

The researchers also looked at the Paycheck Protection Program and found the loans to small businesses had little impact on employment rates. In fact, employment patterns were almost identical among businesses above and below the 500-worker eligibility cutoff. The researchers say recent gains in jobs numbers appear to be the result of an increase in consumer spending partially from the stimulus package and from receding health concerns.

In the report, the researchers also suggest that as time passes the downturn may be driven less by health concerns. If that happens, tools like stimulus payments could have more impact in areas with reduced spending.

“This is the value of having the tracker and the broader theme of what we’re doing here,” Chetty said. “The big picture here is traditionally it’s very hard to do the type of analysis [we just put together] because we haven’t had the data to be able to monitor the economy in such a way before. What we’re trying to do with the Opportunity Insights Economic Tracker is provide tools to essentially answer these questions in real time, so that [we] can see when this shock becomes a traditional economic shock. And not just answering that question at the macro level [but] area by area … Where do we need to try to focus our attention? Which subgroups of people? And so the idea is that by pulling together these private-sector data sources, we can now be able to speak to those questions much more precisely.”